Simple interest and compound interest are two methods used to calculate the interest on a principal amount of money, but they differ in how they calculate and apply that interest. Here are the key differences between the two:

Article continues below advertisement

Calculation Method:

Simple Interest: Simple interest is calculated on the initial principal amount (the original sum of money) throughout the entire period of the investment or loan. The interest is calculated as a fixed percentage of the principal, usually expressed as an annual interest rate.

Compound Interest: Compound interest takes into account not only the initial principal amount but also any interest that has previously been added to the principal. It calculates interest on both the original principal and any accumulated interest over time. This means that interest can grow over time, compounding at regular intervals, such as annually, semi-annually, quarterly, or monthly.

Interest Growth:

Simple Interest: With simple interest, the interest amount remains constant throughout the investment or loan period because it's calculated only on the initial principal.

Compound Interest: Compound interest can grow significantly over time because it's calculated on both the initial principal and the accumulated interest. As a result, the interest earned or owed increases as time passes.

Formula:

- Simple Interest: The formula for calculating simple interest is straightforward:

- Simple Interest = Principal × Rate × Time

where:

Principal is the initial amount of money.

Rate is the annual interest rate (expressed as a decimal).

Time is the time period for which the interest is calculated (usually in years).

Compound Interest: The formula for calculating compound interest is more complex and involves the compounding frequency. The general formula is:

- A = P(1 + r/n)^(nt)

where:

A is the final amount, including both principal and interest.

P is the principal amount.

r is the annual interest rate (expressed as a decimal).

n is the number of times that interest is compounded per year.

t is the time period (in years) the money is invested or borrowed for.

Earnings or Costs:

Simple Interest: Typically, simple interest results in lower earnings for savings or lower costs for borrowing when compared to compound interest, as it doesn't take into account the growth of interest over time.

Article continues below advertisement

Compound Interest: Compound interest can result in higher earnings on investments or higher costs on loans due to the compounding effect, especially over longer periods.

In summary, simple interest is calculated only on the initial principal amount and remains constant over time, while compound interest takes into account both the principal and accumulated interest, leading to a compounding effect that can significantly impact the final amount. Compound interest tends to favor investors and lenders, while simple interest is more straightforward and favors borrowers and those with fixed-rate savings accounts.

What is Simple Interest?

Simple interest is a method of calculating interest on a loan or an investment based on a fixed percentage of the principal amount over a specified period of time. It is called "simple" because it is calculated only on the initial principal amount and does not take into account any interest that may have already accrued. In simple interest, the interest is constant throughout the entire duration of the loan or investment.

Article continues below advertisement

Article continues below advertisement

The formula for calculating simple interest is:

- Simple Interest (SI) = Principal (P) × Rate (R) × Time (T) / 100

Where:

SI is the simple interest.

P is the principal amount (the initial amount of money).

R is the annual interest rate (expressed as a percentage).

T is the time (usually in years) for which the interest is calculated.

For example, if you have a principal amount of $1,000, an annual interest rate of 5%, and the interest is calculated for 2 years, the simple interest would be:

- SI = $1,000 × 5% × 2 / 100 = $100

So, the simple interest on a $1,000 loan at a 5% annual interest rate for 2 years would be $100. This means that after 2 years, you would owe a total of $1,100, including the principal and the interest.

What is Compound Interest?

Compound interest is a concept in finance that refers to the interest that's earned or charged not only on the initial amount of money (the principal) but also on any accumulated interest from previous periods. In other words, it's interest that compounds over time, leading to exponential growth or accumulation of wealth or debt.

Article continues below advertisement

Here's how compound interest works:

Initial Principal (P): This is the initial amount of money you invest or borrow.

Interest Rate (R): The interest rate is the percentage of the principal that is either earned (in the case of investments) or charged (in the case of loans) over a specific period, usually expressed annually.

Time (T): The time represents the number of periods for which interest is calculated. It can be in years, months, or any other time unit.

The formula to calculate the future value of an investment with compound interest is:

A = P(1 + r/n)^(nt)

Where:

A is the future value of the investment/loan, including both the principal and interest.

P is the initial principal amount.

r is the annual interest rate (expressed as a decimal).

n is the number of times interest is compounded per year.

t is the number of years the money is invested or borrowed for.

Compound interest can have a significant impact on the growth of savings or the increase in debt over time. The more frequently interest is compounded (higher "n"), and the longer the money is left to grow (higher "t"), the greater the impact of compound interest. This is why compound interest is often seen as a powerful force for building wealth when investing and a potential burden when dealing with debt. It allows your money to grow or your debt to increase at an accelerating rate.

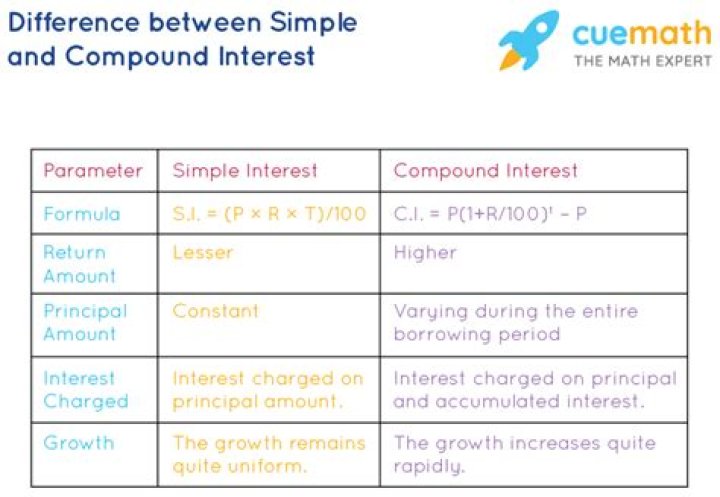

Simple Interest vs Compound Interest

Here is a difference between simple interest and compound interest in tabular column.

Characteristic | Simple Interest | Compound Interest |

Definition | Interest paid on the principal amount only | Interest paid on the principal amount and the accumulated interest of previous periods |

Formula | SI = (P * R * T) / 100 | CI = P * [(1 + R/100)^T - 1] |

Calculation | Straightforward | More complex, requires exponentiation |

Growth | Linear | Exponential |

Return | Lower over time | Higher over time |

Impact of time | Less significant | More significant |

Here is a table showing the difference between simple and compound interest for a principal amount of $1,000 invested for 10 years at an interest rate of 5%:

Article continues below advertisement

Article continues below advertisement

Year | Simple Interest | Compound Interest |

1 | $50 | $50.25 |

2 | $100 | $50.51 |

3 | $150 | $50.78 |

4 | $200 | $51.05 |

5 | $250 | $51.32 |

6 | $300 | $51.59 |

7 | $350 | $51.87 |

8 | $400 | $52.15 |

9 | $450 | $52.44 |

10 | $500 | $52.73 |

As you can see, the difference between simple and compound interest is relatively small in the early years. However, over time, the difference becomes more significant. In the example above, the investor who earns compound interest will have accumulated an additional $27.30 by the end of 10 years.

Compound interest is a powerful force that can help you grow your wealth over time. It is why it is important to start saving and investing early.

Real-Life Applications of Simple Interest and Compound Interest

Simple interest and compound interest are financial concepts that are widely used in various real-life applications. Here are some examples of how they are applied:

Article continues below advertisement

Simple Interest:

Bank Savings Accounts: When you deposit money in a savings account, the bank pays you interest based on the principal amount. This interest is typically calculated using simple interest.

Loans: Simple interest is often used for personal loans or car loans. Borrowers repay the principal amount plus the interest over a predetermined period.

Certificates of Deposit (CDs): When you invest in a certificate of deposit, the bank pays you interest at regular intervals, usually using simple interest.

Renting: In some rental agreements, security deposits may earn simple interest, which is then returned to the tenant when the lease ends.

Bonds: Some bonds pay periodic interest to bondholders using simple interest calculations.

Compound Interest:

Bank Accounts: Compound interest is commonly used in savings accounts and investment accounts. Your interest earns interest, which results in exponential growth over time.

Investments: When you invest in stocks, mutual funds, or other financial instruments, your returns can compound over time, leading to significant wealth accumulation.

Article continues below advertisement

Retirement Accounts: Compound interest plays a crucial role in retirement planning. Retirement accounts like 401(k)s and IRAs allow investments to grow tax-deferred, and the compound interest helps your savings grow over the long term.

Mortgages: Compound interest is used in home mortgages. Over time, borrowers pay interest on the remaining principal balance, which decreases as they make payments.

Credit Cards: Credit card companies use compound interest to calculate the interest owed on unpaid balances. This can result in substantial debt if not managed properly.

Business Investments: Businesses often invest surplus funds in interest-bearing accounts or instruments, and the interest compounds to increase their capital over time.

Education Savings: College savings plans like 529 plans use compound interest to help families save for their children's education expenses.

Real Estate: Investors in real estate can benefit from compound interest when their property appreciates in value, and they reinvest the profits.

Retirement Annuities: Some retirement income plans, such as annuities, provide regular payments that may include both principal and interest, with the interest portion potentially growing through compounding.

In summary, simple interest and compound interest are fundamental concepts in finance and are used in a wide range of real-life financial scenarios, from everyday banking to long-term investments and retirement planning. Understanding these concepts can help individuals make informed financial decisions.

Which one is Better? Simple Interest or Compound Interest

Compound interest is better than simple interest.

- Simple interest is calculated only on the principal amount, while compound interest is calculated on the principal amount plus any accrued interest. This means that compound interest grows exponentially over time.

- For example, if you invest $1,000 at a 10% simple interest rate, you will earn $100 in interest each year. After 10 years, you will have earned a total of $1,000 in interest.

- However, if you invest $1,000 at a 10% compound interest rate, you will earn $100 in interest in the first year. In the second year, you will earn 10% interest on the principal amount plus the interest you earned in the first year, for a total of $110 in interest. And so on. After 10 years, you will have earned a total of $1,610.51 in interest.

- As you can see, compound interest can help you grow your money much faster than simple interest.

- Compound interest is especially beneficial for long-term investments, such as retirement savings. If you start saving early and reinvest your earnings, you can take advantage of the power of compound interest to build a significant nest egg over time.

- Of course, there are also some drawbacks to compound interest. For example, if you borrow money at a compound interest rate, your debt can grow very quickly if you don't make your payments on time.

Overall, compound interest is a powerful tool that can help you grow your money or save money on interest payments. It is important to understand how compound interest works so that you can use it to your advantage.

Article continues below advertisement

Article continues below advertisement

Some Solved Examples on Simple Interest and Compound Interest

Here are some solved examples on simple interest and compound interest:

Simple Interest Examples:

Example 1:

Find the simple interest on a principal amount of $2,000 at an interest rate of 5% per annum for 3 years.

Solution:

Using the formula for simple interest:

Simple Interest (SI) = (Principal × Rate × Time) / 100

SI = (2000 × 5 × 3) / 100

SI = (100 × 3)

SI = $300

So, the simple interest is $300.

Example 2:

How much money will you have if you invest $5,000 at an interest rate of 4% per annum for 2 years?

Solution:

Using the formula for the total amount (A) when interest is compounded annually:

A = P + SI

A = $5,000 + [(5000 × 4 × 2) / 100]

A = $5,000 + $400

A = $5,400

So, you will have $5,400 after 2 years.

Compound Interest Examples:

Example 1:

Find the compound interest on a principal amount of $2,000 at an interest rate of 6% per annum compounded annually for 3 years.

Solution:

Using the formula for compound interest:

A = P(1 + r/n)^(nt)

Where:

A = the final amount

P = principal amount

r = annual interest rate (in decimal form)

n = number of times interest is compounded per year

t = time (in years)

In this case, P = $2,000, r = 6% or 0.06, n = 1 (compounded annually), and t = 3 years.

A = 2000(1 + 0.06/1)^(1*3)

A = 2000(1.06)^3

A ≈ 2000(1.191016)

A ≈ $2,382.03

Now, to find the compound interest:

Compound Interest (CI) = A - P

CI = $2,382.03 - $2,000

CI ≈ $382.03

So, the compound interest is approximately $382.03.

Example 2:

If you invest $10,000 at an interest rate of 5% per annum compounded semi-annually, how much will you have after 4 years?

Solution:

Using the formula for compound interest:

A = P(1 + r/n)^(nt)

In this case, P = $10,000, r = 5% or 0.05, n = 2 (compounded semi-annually), and t = 4 years.

A = 10000(1 + 0.05/2)^(2*4)

A = 10000(1 + 0.025)^8

A ≈ 10000(1.219065)

A ≈ $12,190.65

So, you will have approximately $12,190.65 after 4 years.

These examples should help you understand how to calculate simple interest and compound interest in various scenarios.